Bring you thought-provoking stories about Bitcoin and the cryptocurrency revolution. Here to help educate the community and bring others up to speed! Vires in Numeris.

Consumer Banking Takes Major Step Forward With Blockchain Technology To Help Consumers Save

Get link

Facebook

X

Pinterest

Email

Other Apps

This post was originally published on my Medium blog on November 30th, 2017 and can be found here. I hope you enjoy and find this helpful!

Most of us have consumer bank accounts that we use to pay our bills, make purchases, investments, and save money with — transfer and store value. Signing up for a bank account requires documentation of our personal and ID information. Operating our bank account requires us to log-in to an online banking portal where our information is stored. Have you ever actually looked at your bank statement to see how much the bank rewards you for storing your value with them?

In this article, I will:

- briefly dive into the statistics, painting the harsh reality of the current mainstream consumer banking savings return rates (Chase & Wells Fargo);

- take a look at Goldman Sachs’ consumer Certificate of Deposit (CD) product; and

- dive into an innovative project aiming to change the way we transfer and store value.

Banks offer consumers saving accounts to give us a separate account to store our value aside from our spending account, earning an interest rate for doing so. Consumer savings accounts only earn interest when the funds are in the account, but afford consumers the ability to transfer funds out of their account in needed. Did you know savings accounts are limited to only 6 outgoing transfers per month (Regulation D)? Consumers are charged a fee if they exceed 6 transfers in 1-month, Bank of America charges a $10 fee for each outgoing transfer after 6 in the 1-month period.

Let’s take a look at Wells Fargo’s consumer saving rate above. This might be disgruntling news to you if you do not scan your savings account statement, but mainstream banks only offer (in the US at least) 0.01% interest rates — for every $100 you save and store in your savings account. At the end of one-year you will have earned $0.01 for your untouched, $100 savings.

Let’s not forget about JPMorgan Chase Bank as they have been in the mainstream news quite a bit recently in association with contrasting views on Bitcoin and blockchain technology. Looking at the consumer savings account interest rates above, straight from their website, we see some nice disclosures before we can get to their interest rate number..

Hey, at least Chase is disclosing they have the power to take advantage of us at will, right? Are you starting to see why it is in the banks’ best interest that ‘Bitcoin is a fraud’?Banks make money by charging us fees and loaning us money when we need it, charging an interest rate on the amount loaned to us.

Above is the September 12th, 2017 video of JPMorgan Chase Bank CEO, Jamie Dimon, talking about Bitcoin a fraud and bubble, comparing it to the infamous Tulip Mania (Investopedia Explained) if you haven’t yet listened.

Let’s look at Goldman Sachs’ CD rates below:

Certificate of Deposits — A Harsh Reality

Goldman Sachs’ Consumer Certificate of Deposit Accounts: Source

The major difference between a savings account and certificate of deposit (CD) is that you cannot remove funds locked in a CD without paying a penalty fee. Due to this restriction, consumers are rewarded ‘much higher’ interest rates than consumer savings accounts offer.

Look at those CD rates! Even locking your funds into a CD for the minimum of 6-months earns the saver 60x rate compared to a savings account!I am being a bit sarcastic as locking in $100 into the 6-month CD would earn the consumer a $0.30 at the end of the 6-month period. Unfortunately, even the 0.60% interest rate falls far below the average US rate of inflation of 2.2%. This means 12-months from now, your $100 only has $97.8 of buying power due to the rate of inflation devaluing the currency your savings are denominated in.

Does it make sense to earn $0.01 if your $100 savings are decreasing in value by $2.2? Take notice they are advertising the 5-year, 2.40% rate on across the internet.

Conclusion About Bank Sentiment Toward Blockchain Technology

Jamie Dimon’s Tulip Mania statement breaks some of the most basic economic principles. For instance, is there a limited supply in existence? What utility do Tulips carry?They smell good or look pretty? So they had absolutely no utility and people could grow them in their back yard…Tulips are also organic material so they would deteriorate over time — definitely not a safe store of value. The Tulip Mania bubble was just the most pronounced speculative bubble example humanity have ever seen.

Ultimately, it sounds like banks are nervous that Bitcoin and blockchain technology are enabling consumers to be in complete control of their value storage and transferring — heavily taking away from their revenue source…what will they tell investors when they fail to meet expectations? Let’s look at just how this technology is causing banks to react this way.

MinexBank — Fair Rates, Value Appreciation and 100% in Your Control

MinexCoinlaunched their Initial Coin Offering on May 16th, 2017 on a mission to create a new era of payments based on their low-volatility cryptocurrency through MinexBank. The team successfully raised 287 BTCfrom 1,981 participants at the time. MinexCoin has its own hybrid Proof-of-Stake and Proof-of-Work blockchain — it’s not a token on the Ethereum blockchain. Because they created their own blockchain, the MinexCoin ledger is completely separate from that of other blockchains who have their own blockchain network — Bitcoin, Ethereum, NXT/ARDR, NEO, Ripple, and Dash are examples of separate blockchain networks.

Just recently, the team launched their MinexBank system which allows users to have full control over their coins while earning an interest rate of ‘parking’ coins for set amounts of time, similar to that of a Certificate of Deposit. The major differences here are:

- your value is stored in MinexCoin (MNX);

- you have full control over your physical funds, stored on your hardware device; and

- you are not charged a fee for withdrawing early — you just miss out on the interest you were supposed to gain for the period if breaking the ‘parking period.’

Creating a Generation of Savers — Quick Run-down of MinexCoin Ecosystem Components’ Importance

First off, the MNX are stored on your computer in the MinexWallet. This means the coins are physically on your hardware device. If it breaks and you have not backed up your wallet.dat file, you will lose all of your coins forever. Yes, blockchain technology requires the user to have be responsible for their own funds. To download the MinexWallet, users would go to the official MinexCoin website and download the wallet that fits their operating system (image above).

After downloading the MinexWallet, encrypting it, backing it up, and generating your public account address — you can use it to send and store your coins on your laptop, computer, or whichever hardware device you downloaded it to. Next, users must open a MinexBank account. This link leads you to their ‘how-to guide.’

Notice how the only information asked for upon account opening is your public MinexCoin address and the creation of your account password?

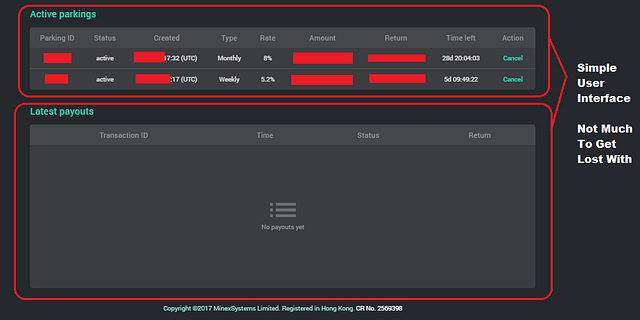

Above is the User Interface for the online MinexBank ‘parking portal.’ Notice how simple it is? No accounting-style balance formatting. No debits and credits. Nothing very confusing at all, but have you gone into your online bank account portals? There is so much information it is overwhelming and not very function. MinexBank is opposite — focused on functionality with very little supplemental information for users to get lost in.

As you can see above, you have the real-time status of your parked coins; the amount parked with it it’s corresponding interest rate; and the real-time duration of time left until the number of coins are usable and the interest is earned. The interest rate above is not APY either — it is simple interest.

For example, those ‘parking’ 100 MNX at the 8% monthly interest rate will receive 8 MNX at the end of the month, sent to the wallet on their hardware device. Simple as that.

Your account cannot overdraft. MinexCoin/MinexBank will not charge you fees. They are not using different types of interest rates in advertising to confuse you. None of that crap. Instead, they are focused on the User Experience and product functionality…something banks clearly lack in 2017.

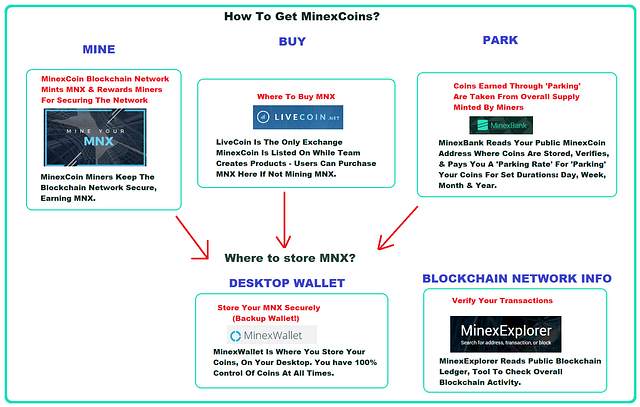

Just to clarify and make this easier to understand for those of you who understand better with a visual. MNX is minted by miners when they mine blocks and by ‘parking’ coins (interest) paid out to those who park them. The coins minted through parking take away from the overall amount of coins minted through the mining process, controlling the supply to keep them on pace to have a limited maximum supply of 19,000,000 MNX.

Banks Strategically Create Their Systems To Make Money Off Us

I would say the reason banks lack easy UI is because banks created their system in a way that preys on our lack of knowledge, charging us astronomical fees at various points of their product system:

- Information over-load in online portal makes it hard to find answers and navigate.

- Automatic payments for ‘convenience’ only makes tracking personal finance more difficult if consumer is not financially savvy.

- $35+ overdraft fees for accidentally going -$0.50 on accounts — goes hand-in-hand with their automatic payment product.

- $10 fee for conducting more than 6 transfers/withdrawals out of your savings account — Regulation D forces banks to do this, but they do not do a great job of conveying the regulation to consumers.

- “Rewarding” us a 0.01–2.40% max interest rate for storing our money with them while they use that money to charge astronomical interest rates whenloaning to others who are in need of the funds.

- FDIC insured accounts give you more confidence storing your money with them, all while inflation destroys your spending power year-over-year.

- Charging consumers fees just for having bank accounts with them — debit/checking AND savings account service fees…

These are just a few of the tactics employed by the mega-banks across the world to continue churning out profits for their investors. It’s a broken system and should not be hard to catch a glimpse of after reading this article.

I do this for you and the rest of humanity. My work is fueled by passion which comes through many bad personal experiences with the financial system as we know it, which feeds into every other facet of our lives — everything in life is driven by value and fiat currency is simply a mode of value transfer, just like MinexCoin. The old system is broken, MinexCoin is creating a more equitable system for us all.

Hope you enjoyed this piece! Follow along as I continue to share my perspective on how cryptocurrency and blockchain technology are creating a more fair Earth!

Below are some resources for beginning cryptocurrency enthusiasts or others interested in something new: The links below include affiliate/referral links which help support me as a writer. I do not get paid to write and this is my only means to generating income for writing. Thank you in advance and hope these resources are helpful to you. I only include resources in this list that I have used in the past.

- Cryptoversity by Chris Coney — The Online School That Pays You To Learn About Bitcoin, Crypto-currencies and Blockchains

- HitBTC Exchange— major exchange, access ICOs and multi-currencies.

- CoinTracking — Your personal Profit / Loss Portfolio Monitor and Tax Tracker for all Digital Coins

- Changelly — as easy as purchasing cryptocurrency gets — watch the exchange rate.

- Exmo Exchange- just launched their own coin and adding robust features to the trading platform.

- CoinMate.io — Bitcoin exchange/arbitrage made easy.

- CEX.io— Buy Bitcoin w/ credit card, ACH bank transfer, SEPA transfer, cash, or AstroPay. Credit purchases are instant.

- CoinPayments — Receive payment via 70+ different cryptocurrencies — the crypto-PayPal.

- CoinMama — purchase Bitcoin and Ethereum w/ credit/debit cards & using cash through WesternUnion on their platform. Best for Euro purchases.

- Bit-Z— Newer Top 20 cryptocurrency exchange adding new, ICO coins all the time.

- Gate.io--Cryptocurrency exchange listing new coins - get 10% off trading fees if you register with this link.

- CryptoPay— Spend your crypto. Can order a Euro, US Dollar or Pound crypto-debit card. Get 25% off using this link.

- LinkCoin— Your ticket to using LinkCoin, Bibox, and Bibox365 exchange products and ICO’s — mainly Asian cryptocurrencies that are not available on other exchanges.

I am the author of this article and the original piece of content can be found here on my Medium blog . At the end of last year, I wrote an article entitled Binance Exchange: Fueling a Hot New Era of Token-based Exchange Models? , diving into the innovative token-based exchange model Binance brought to the competitive table. Unarguably, their business model along with being at the right place and time has catapulted them to being the top cryptocurrency exchange in the world — 7-months after starting the business. This is unheard of in the world of business . A startup becoming the all hailed unicorn within MONTHS. Unicorn = billion dollar valuation . I don’t know what Binance’s valuation is or if we can even value the organization from a traditional valuation standpoint; however, their 24-hour volume as I type this is $3.9 billion . They charge a 0.10% trading fee — we’ll do the math further down. This comes ...

I am the author of this piece of content and the original can be found on my Medium blog here . Hello! As you may have heard, NEO Blockchain has been considered the ‘Chinese Ethereum’ for about a year now since the project re-branded from Antshares. This is because NEO will perform similar functions as Ethereum does as a platform for decentralized applications with smart contract capabilities, among other tech integrations. NEO’s NEP-5 token standard is synonymous to Ethereum’s ERC-20 token standard in terms of what they mean to the individual networks. Since the inception of ERC-20, there have been over 85,000 tokens created on the Ethereum blockchain network , just under that particular standard. This is a major focus in NEO’s growth strategy, but instead of taking Ethereum’s radically decentralized approach, NEO grows stronger with regulatory compliance standards — meaning, NEO is poised for institutional capital to f...

Image Source Virtual reality continues to be a hot topic in the world of tech as more startups are formed and new technologies see the early days of VR integration. Those of us operating on a day-to-day basis in the cryptocurrency community understand the power of blockchain tech while exhibiting an explosion of startups leveraging VR to raise capital via initial coin offering. However, nothing quite measures up to the uniquely creative virtual platform that Decentraland has become along with other innovative projects like CryptoKitties. Digital objects now gain an identity through blockchain and other technologies integrating with virtual reality will allow for a deeper immersive experience. One example of a technology which will be able to integrate with VR are projects utilizing the Non-fungible Token (NFT) standard, ERC-721, which is turning out to be quite an interesting development. CryptoKitties is an example of a Non-fungibl...

Comments

Post a Comment